April 24, 2026 – to be fair, i've been seeing some buzz on the timeline.

There is a particular kind of cognitive dissonance that comes from watching the most structurally significant twelve months in crypto's short history unfold against a backdrop of almost universal apathy.

That's where we are. Right now. Today.

Scroll any feed. Open any group chat. The prevailing emotion isn't exactly fear. It's closer to resignation. A kind of practiced detachment from price action that has curdled, in some people, into genuine disengagement from the space entirely. The tourists left. Some of the believers left too. What remains is a market populated largely by participants who are either constitutionally immune to drawdown, institutionally obligated to stay, or so deep in conviction positions that exit is no longer a psychological option available to them.

I'm one of the latter. Which means I've spent the last few months marinating in a very specific flavour of cognitive dissonance: the growing gap between what I see being built and what the feeds are telling me to feel.

Like and retweet if you find value in this article. Subscribe to future issues here. Thank you!

The Objective Case: Why the Foundation Has Never Been Stronger

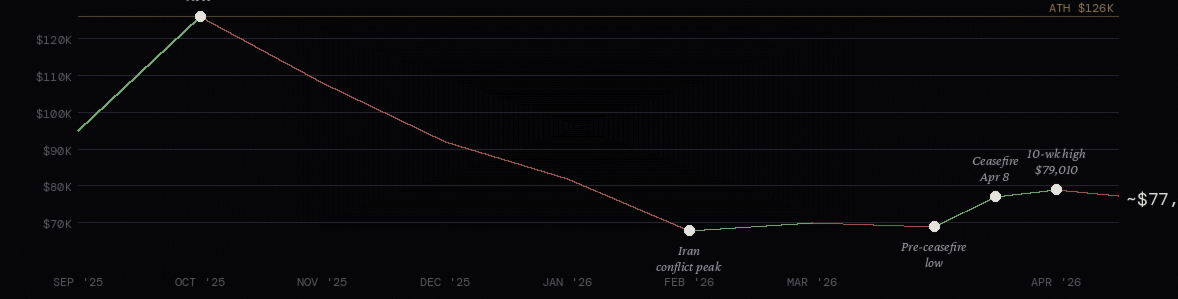

A year ago, March 2025, we were in the middle of a choppy consolidation — Bitcoin ranging through the $80,000s, ETH struggling to hold $2,000, the euphoria of the ETF launch period well behind us and the real ATH still months ahead. The meme cycle was trying to find its footing. The market was waiting for something.

It found it. Bitcoin hit a new all-time high in October 2025, touching $126,000. The cycle finally delivered. And then — with the particular cruelty that only crypto markets can manage — it started taking it back almost immediately. A brutal five consecutive red monthly candles later, the drawdown reached 44% from peak. Since then — partly on the back of a US-Iran ceasefire and a wave of institutional buying that culminated in Strategy’s $2.54 billion single-tranche purchase in April — Bitcoin has clawed back to roughly $77,000, trimming the drawdown to around 39% from ATH. With a trade war overhead and a Fed still on pause, we find ourselves here.

What's strange is that the drawdown has coincided with, and in some ways been obscured by, a period of genuine institutional and protocol-level maturation that should, on any rational medium-term horizon, be extraordinarily bullish.

Consider the facts as they sit today.

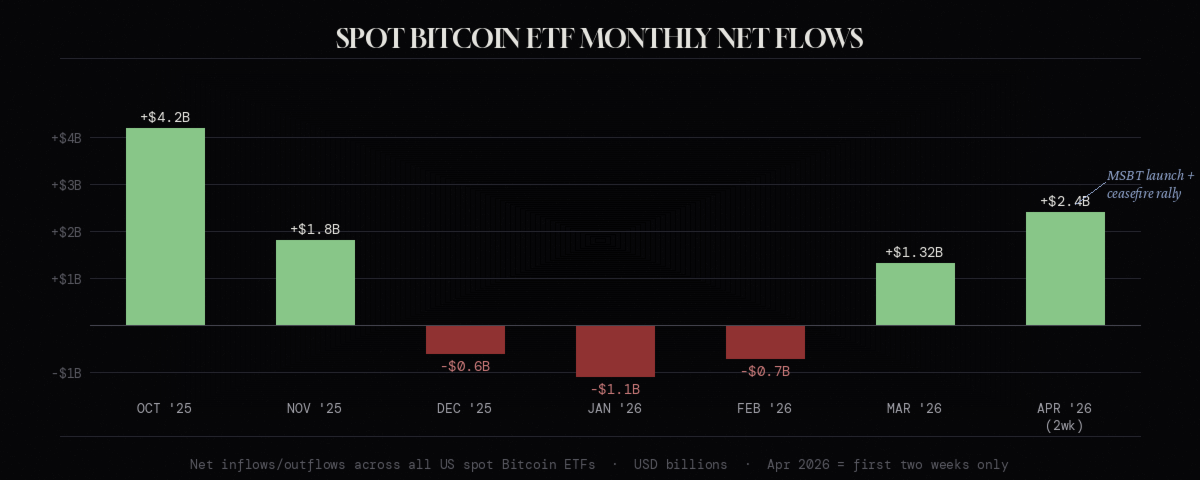

The ETF bid — the mechanical, institutional floor that defines this cycle’s structural difference from every prior one — told the real story of the past three months in three acts.

January and February were brutal: the category shed approximately $1.8 billion in net outflows as Bitcoin sold off from its October highs and macro headwinds compounded.

Then March arrived, and the bid returned — Bitcoin ETFs posted their first positive monthly inflows of 2026, absorbing $1.32 billion.

April has been more dramatic still: spot Bitcoin ETFs logged $2.4 billion in net inflows in less than two weeks, with the ceasefire-driven risk-on rotation and Morgan Stanley’s MSBT launch on April 8 — the first spot Bitcoin ETF from a major US bank — providing fresh distribution channels.

- MSBT attracted $34 million on day one and crossed $100 million in its first week, Morgan Stanley’s strongest ETF launch on record.

- Total net assets across the category have climbed back toward $95–100 billion.

- The Grayscale outflow overhang — which haunted the 2024 ETF launch period — has nearly evaporated, with GBTC bleeding at a fraction of its earlier pace.

That’s not nothing. That’s a structural floor being quietly constructed while everyone stares at the price.

Then there's the stablecoin story, which has arguably been the most underappreciated macro development in the space (at least by CT natives).

- Total stablecoin market capitalisation doubled between January 2023 and January 2026 to reach $308.55 billion.

- Annual transfer volume reached approximately $33 trillion in 2025. For context, the GENIUS Act was signed into law in July 2025.

- The GENIUS Act created the first federal stablecoin framework, bringing regulatory clarity that, as SVB has noted, accelerated the arrival of non-USD stablecoins and opened the door for a new wave of institutional issuers.

Protocols that a year ago were called "interesting experiments" are now operating at scales that make legacy TradFi infrastructure look arthritic. But more on that shortly.

The point is simply this: on the dimension that matters most — real usage, real capital, real infrastructure — the space is better than it was one year ago.

Materially, structurally, undeniably better. If you were designing crypto from scratch and someone handed you today's landscape versus March 2025's, you would take today's without blinking.

On Apathy, and How We Got Here

So why does it feel like a funeral?

Partly, the macro. Trump’s tariff escalation and the Iran war that erupted in earnest at the end of February did real damage to risk appetite globally. The drawdown from the October ATH touched 44% at its worst. Since the US-Iran ceasefire was announced on April 8 and extended indefinitely on April 22, Bitcoin has recovered to around $77,000 — trimming the drawdown to roughly 39% — but the scars from five consecutive red monthly candles are still visible in sentiment data.

But I think the apathy runs deeper than that. It's structural. We are between narratives.

The ETF narrative has been digested. The "institutions are coming" thesis is now simply true — and paradoxically, its truth makes it less exciting. Institutional capital doesn't tell stories. It allocates, dollar-cost averages, rebalances. It moves slowly and it doesn't post about it. The retail participation that generates the manic energy of bull cycles is largely gone — not for fundamental reasons, but because it lost money and went away. Reflexivity works in both directions.

There's also the geopolitical weight. Bitcoin dropped below $69,000 on Sunday as the US, Israel and Iran traded fresh threats and attacks, with Ether losing nearly 5% to sink toward $2,050. Whatever you believe about Bitcoin as a long-term sovereign hedge, the short-term reality is that it remains, in the eyes of most allocators, a risk asset. When equity desks de-risk, they sell crypto alongside everything else. During the February 2026 market stress driven by the Iran conflict, Bitcoin dropped alongside equities rather than functioning as an uncorrelated hedge.

The participants who understand the nuance — that these conditions are precisely the ones that historically precede bitcoin's most violent upward moves — are holding. Everyone else is either flat or in cash, watching from the sidelines, waiting for a signal that may not come in the form they expect.

This is what apathy looks like from the inside.

The Antidepressant POV: Revisiting Q1 Catalysts That Deserve Your Attention

Before you reach for the existential dread, allow me to administer some intravenous hopium — distilled, no fillers, straight from the protocols themselves.

BlackRock ETHB: The Structure Changes

On March 12, BlackRock launched the iShares Staked Ethereum Trust, trading under the ticker ETHB on Nasdaq — the firm's third crypto ETF and its first to incorporate staking. ETHB stakes between 70% and 95% of its Ethereum holdings, with investors receiving approximately 82% of gross staking rewards, currently running at roughly 3.1% annually, distributed monthly.

This sounds incremental. It is not.

Every prior crypto ETF in the United States was a passive price-tracking instrument. ETHB changes the fundamental value proposition: Ethereum is now, for the first time, accessible to traditional portfolio managers as a yield-generating asset. Not speculative beta — yield. The same logic that makes a bond interesting to a pension fund, the same calculus that governs how institutions evaluate income-producing instruments, now applies to ETH.

What changes with ETHB is the scale of distribution behind it. BlackRock manages over $130 billion across crypto-related ETPs, and iShares captured 95% of all digital asset ETP flows in 2025. When BlackRock validates a structure, the rest of the industry follows. The template is now set. Solana, Cardano, Polkadot staking ETFs are in the queue. The domino effect is structural and it has already begun.

Bitcoin as a Sovereign Hedge: The Slow Burn Thesis

The Iran war has, counterintuitively, been a case study in Bitcoin's evolving nature. The consensus narrative — "Bitcoin is correlated to equities and will dump with everything else" — has been partially, interestingly, wrong.

Since the ceasefire broke the conflict, the data has been instructive. In the immediate aftermath of the April 8 ceasefire announcement, BTC surged 5% to $72,700 in under 24 hours — faster than the S&P 500 and Nasdaq recovered. Bitcoin has since hit $79,010, its highest level in 10 weeks. Through the full arc of the conflict — outbreak to ceasefire — Bitcoin outperformed equities on a net basis. Wars are expensive. Financing them requires more government borrowing, which expands deficits, increases liquidity, and weakens the dollar. Exchange reserves have fallen to approximately 2.21 million BTC — a level not seen since December 2017 — as Bitcoin migrates into long-term storage, ETF custody, and self-custody wallets. Strategy (formerly MicroStrategy) just disclosed its largest single Bitcoin purchase since 2024: 34,164 BTC for $2.54 billion, bringing its total holdings to 815,061 BTC. The quiet hands are buying. They always are, in environments exactly like this one.

ETF Flows: The Recovery

After a brutal start to 2026 — $1.8 billion in net outflows through January-February — the institutional bid has returned with conviction. March delivered $1.32 billion in net inflows, the category’s first positive month of the year.

April has surpassed it: $2.4 billion in less than two weeks, with BlackRock’s IBIT absorbing the bulk and Morgan Stanley’s newly launched MSBT adding a fresh demand channel with 16,000 financial advisors and $9.3 trillion in client assets now able to direct allocations toward Bitcoin through a proprietary product.

US Admiral Samuel Paparo told Congress in April that Bitcoin “shows incredible potential” as a strategic tool in the China rivalry. The Fear and Greed Index is still registering extreme fear. The flows don’t care. The floor is being built, brick by brick, in the dark, while sentiment indices are screaming.

We Might Not Recover Right Away — And That's Fine

I won't be overly optimistic, nor will I be naive about the headwinds.

The Iran conflict remains genuinely unresolved. Reported strikes on Iran's Natanz nuclear facility and the Kharg Island oil hub represent the broadest Middle Eastern conflict in decades, and the market has not priced in a full escalation scenario. Every time talks surface, risk-on returns; every escalation headline, we give it back. This ping-pong between $68,000 and $77,000 may continue for weeks – or we might just be on the brink of recovery. NFA as always.

Separately, tariffs. The global trade war remains a live variable, even if the oil shock from the Iran conflict is fading. A Fed still caught between residual energy inflation and slowing growth is a Fed that stays on pause — and a Fed on pause is a Fed that isn’t creating the macro liquidity expansion that crypto bull markets historically feed on. Watch the April 28-29 Fed meeting: if the committee signals any hawkish tilt, the recent recovery rally could give some back.

There's also the quiet matter of altcoin devastation. If you've been holding a diversified bag of mid-caps through this cycle, you are not just down — you are, to put it bluntly, holding assets that WILL NOT meaningfully recover.

The capital rotation thesis that lifted everything in 2021 hasn't fired. Layer 1 competition has fragmented attention and liquidity. Many projects have simply died a sad death from a lack of funding.

The honest read: we are not on the eve of a V-shaped recovery. What we are on the eve of is a multi-month accumulation phase in which the underlying fundamentals silently become more compelling with each passing week — until, suddenly, they aren't silent anymore.

Or I might be bullshitting you and we'll be back to 6 fig bitty in a few months. Don't do leverage.

What We're Actually Excited About

The real story of this cycle — the one that doesn't show up in price but will eventually — is happening at the protocol layer. Let me tell you what I've kept watching, starting with the obvious one.

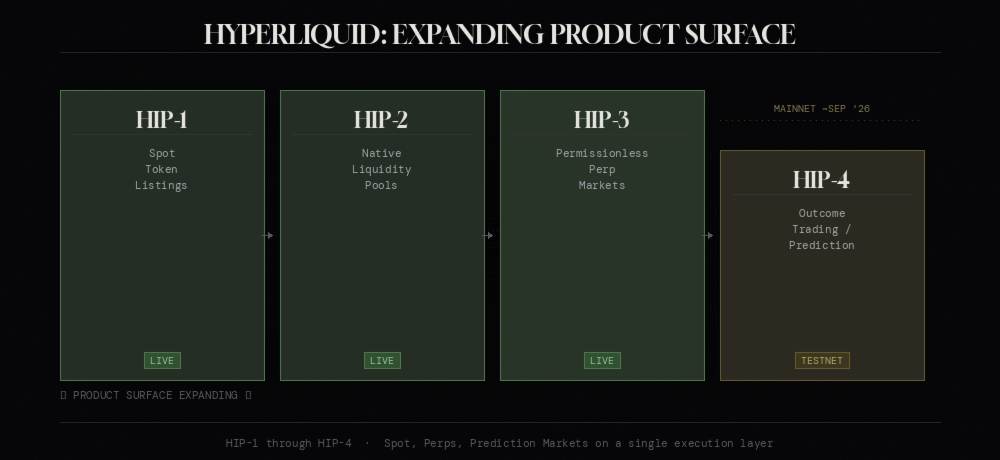

Hyperliquid: 247 Markets and the Prediction Machine

Hyperliquid has become one of those rare cases where the protocol is simply executing at a level so far ahead of its competitors that the question isn't whether it keeps winning, but how large the eventual gap becomes.

They processed over $225 billion in trading volume in January 2026 alone. The HIP-3 upgrade unlocked permissionless perpetual markets — equities, gold, FX — allowing anyone to create a market by staking HYPE tokens. 247 markets and counting.

Then came HIP-4. On February 2, Hyperliquid announced outcome trading — fully collateralized contracts that settle within a fixed price range, designed for prediction markets and options-like products. The announcement sent HYPE up over 20% in a single day, in a market where everything else was bleeding.

The strategic significance here is easy to underestimate. CFTC Chairman Michael Selig has signalled the agency is preparing a new rulebook for prediction markets, as platforms like Polymarket and Kalshi draw billions in activity.

Hyperliquid is positioning itself to absorb this entire category by making outcome contracts a native primitive — composable with perpetuals, denominated in USDH, accessible to the same capital base that already lives on HyperL1. As of April 2026, HIP-4 prediction markets remain on testnet — mainnet is confirmed “within 2026” but no specific date has been set. Polymarket traders currently price September 30 as the most likely launch window. Bitwise has updated its spot HYPE ETF filing (ticker BHYP) with a 0.67% fee — a step Bloomberg’s Eric Balchunas notes often precedes a launch — with Grayscale and 21Shares having also filed.

This is not just something like Polymarket with better UX. This is prediction markets being embedded into the deepest on-chain derivatives stack that exists. The implications are pretty big – pre-IPO markets, political markets, macro event trading — the surface area is vast.

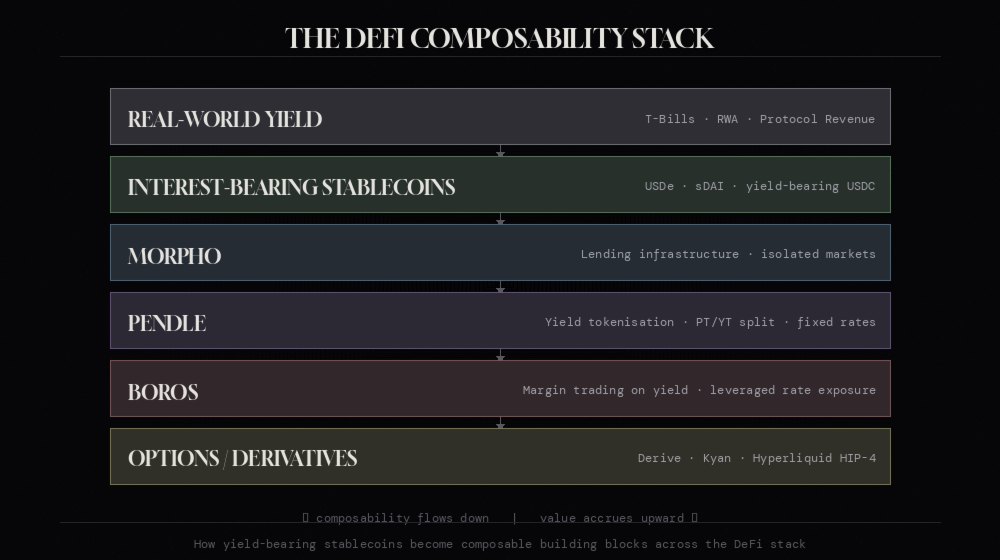

Pendle, Boros, and the Rate Market Infrastructure

Yield markets are the unglamorous backbone of mature financial systems. The fact that on-chain versions of them are finding genuine product-market fit in 2026 is, to my mind, one of the most underrated stories in DeFi.

Pendle's growth reflects the broader expansion of yield-bearing stablecoins, which have surged from $1.5 billion to over $11 billion in the past 18 months. Stablecoin TVL on Pendle has jumped over 60x during the same period. Today, 83% of Pendle's TVL sits in stable assets. The protocol has quietly become the fixed-income desk of DeFi — letting sophisticated users separate principal from yield, express duration views, lock in fixed rates. Duration trading matured, and "on-chain fixed income" became more legible through stablecoin-centric collateral and more structured rate exposure.

Boros — Pendle's expansion into margin trading on yield — is the next chapter of this thesis: using yield exposure not just as a passive allocation but as an actively tradeable instrument with leverage. It's the kind of product that won't make headlines until it has hundreds of millions in open interest. Then everyone will want to write about it.

This is how financial primitives actually get built. Not with fanfare. With compounding.

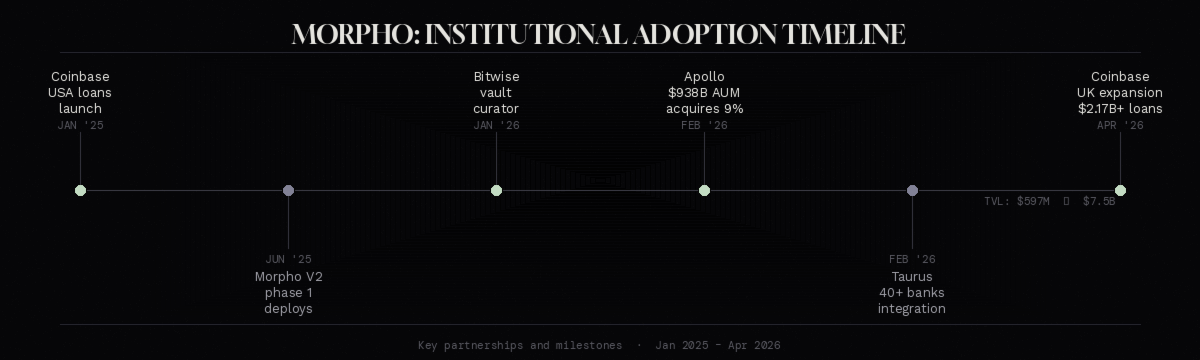

Morpho: The Disconnect That Defines the Opportunity

If I had to identify one protocol where the gap between what the market prices and what the data shows is most pronounced, it would be Morpho. By a wide margin.

Morpho is the second-largest DeFi lending protocol with approximately $7.0–7.5 billion in TVL, up from $5.8–6.8 billion at the time of writing. Its architecture — isolated lending markets, permissionless deployment, curator-managed vaults — has proven to be almost perfectly suited to the institutional DeFi moment we are entering.

Apollo Global Management, which manages over $938 billion in assets, signed a strategic cooperation agreement with Morpho in February 2026 to acquire up to 9% of the MORPHO governance tokens over four years. In the same month, Taurus, which provides custody services to more than 40 banks, integrated Morpho into its custody platform, enabling traditional financial institutions to directly allocate funds to Morpho Vaults within existing compliance frameworks.

Bitwise launched its internally managed non-custodial vault curator service on Morpho in January 2026. Coinbase, meanwhile, chose to use Morpho as the backend for its USDC lending and asset-backed loan products — a "DeFi mullet" model where the frontend is familiar fintech and the backend is Morpho-powered DeFi.

TVL surged roughly 3x year-on-year in ETH terms. Apollo is systematically acquiring governance tokens. The largest exchange in the US is using Morpho as its lending infrastructure. The MORPHO token, at time of writing, does not reflect any of this. That is the opportunity. Not because the token should go up — tokens should always be treated with skepticism — but because the protocol is demonstrating exactly the kind of PMF that, historically, the market eventually notices.

Morpho V2, deployed in phases through 2025 and continuing into 2026, introduces market-driven interest rates — transitioning the protocol from protocol-dictated formulas to the kind of rate discovery mechanisms that traditional credit markets already use. It is, in essence, the on-chain version of how institutional lending actually works. The timing, with Apollo now a governance stakeholder, is not coincidental.

In April, Coinbase expanded its Morpho-powered USDC loan product to the United Kingdom, marking the first international rollout of what has already generated over $2.17 billion in US loan originations. The protocol’s fee velocity is growing at 13.6% week-on-week as of mid-April, and one credible analyst argues it is on pace to overtake Aave in fee revenue within six months — without competing on TVL.

One note of caution: the KelpDAO exploit of April 18, which drained $292 million via a misconfigured LayerZero bridge and shed $13 billion from DeFi’s total TVL, hit Morpho’s TVL by approximately 9.6% in the aftermath. Morpho’s isolated market design limited direct contagion, but the incident is a reminder that the DeFi stack is only as strong as its weakest cross-chain link. 2026 is tracking to be the worst year on record for hacks.

Stablecoins as DeFi Building Blocks

The stablecoin story is not just a payments story. That framing is too narrow, and it obscures what's actually interesting.

Yield-bearing stablecoins maintain a price peg while generating returns from reserve deployment — and their market cap has tripled in the past year, now making up over 4% of the total stablecoin market. Protocols like Ethena's USDe, Pendle's yield-tokenised stablecoins, and the interest-bearing collateral flowing through Morpho vaults are converging into something genuinely novel: a composable, programmable dollar layer that generates yield and functions as collateral and enables rate speculation.

This is the DeFi stack eating itself in the best possible way. Interest-bearing stablecoins become collateral on Morpho. That collateral gets yield-tokenised on Pendle. The yield gets leveraged on Boros. Each layer adds density and utility. The system becomes more expressive with every new primitive that finds adoption.

We are nowhere near the end of this particular trajectory.

Options: The Derivatives Category Finally Arriving

For years, crypto options were structurally broken — dominated by Deribit, illiquid in the tails, inaccessible to on-chain capital, and frankly unusable for most DeFi participants. The category has always felt like it was supposed to matter but somehow never did.

That is changing. Derive and Kyan represent two different but complementary approaches to finally making on-chain options work. The core insight they share: options need to be native to the same capital environment where the rest of DeFi lives. Siloed options platforms can't compete with the composability of systems that allow options positions to interact with lending collateral, yield positions, and perp books within the same margin framework.

HIP-4 on Hyperliquid is, in part, this story. The "outcome contract" primitive is, structurally, an options-adjacent instrument — bounded, fully collateralized, dated. A non-option alternative for what Derive and Kyan are building, HIP-4 is beginning to build into the HyperLiquid stack. The goal is somewhat similar for crypto-natives: an on-chain environment where sophisticated derivatives strategies are executable without the operational overhead and counterparty risk of centralised options venues.

Options prove market fit slowly, then suddenly. We may be approaching suddenly.

The Read

The dichotomy is evolving. Sentiment remains deeply depressed — the Fear and Greed Index is still registering fear even as Bitcoin trades near $77,000.

The ceasefire has shifted the immediate macro backdrop, but the structural headwinds — tariffs, a Fed on hold, altcoin devastation, a KelpDAO-sized reminder that DeFi security is not solved — haven’t disappeared. Bitcoin is down 39% from its ATH and still hasn’t reclaimed $80,000 on a sustained close.

Recovery is happening. It isn’t complete.

And yet. The infrastructure being built right now — yield-bearing stablecoins as composable building blocks, Morpho as institutional lending backbone expanding internationally, Hyperliquid as the on-chain derivatives stack for everything (with HIP-4 on testnet, ETF filings advancing), Pendle and Boros as the rate market layer, Kyan and Derive finally close to finding their moment — is more coherent, more interconnected, and more genuinely useful than anything that existed at the top of the last cycle.

That’s the dichotomy. And sitting inside it, uncomfortable but convicted, is exactly where I want to be.

We'll be here every issue.

— Detached

Nothing in this publication constitutes financial advice. Detached is an independent publication. Do your own research u goofy goobers.